February Freight Trends: Navigating a Sea of Uncertainty

February data from Cass Information Systems demonstrated a promising recovery in freight volumes after weather-induced setbacks in January. Freight volumes climbed 10.5% month-over-month in February, yet they remain under last year's levels, showing a 5.5% year-over-year decrease. This shift was partially due to normal seasonality, recovery from the harsh weather, and pre-tariff imports by shippers. Despite the monthly improvement, the scenario is not entirely optimistic.

Freight Recovery and Seasonal Adjustments

Seasonally adjusted figures reveal that February shipments rose only 4.9% sequentially. This cautious rebound highlights the underlying challenges facing the freight market. Looking into March, the usual peak freight month of Q1, uncertainties surrounding trade policies could derail progress. If seasonal patterns persist, the shipments index could witness a 3-4% year-over-year decline, implying only a modest 2% sequential increase.

Table: Cass Information Systems

| | y/y | 2-year | m/m | m/m (SA) |

|----------------|-------|--------|-------|----------|

| **Shipments** | -5.5% | -9.7% | 10.5% | 4.9% |

| **Expenditures** | -4.6% | -23.4% | 3.6% | -0.3% |

| **TL Linehaul Index** | 1.9% | -3.6% | 1.2% | NM |Expenditure and Rate Dynamics

The freight expenditures dataset from Cass, accounting for total freight spend including fuel costs, recorded a 3.6% sequential rise (but a -0.3% drop when seasonally adjusted) yet decreased 4.6% year-over-year. Notably, retail diesel prices fell 9% compared to the previous year. Shipments fell 5.5% yet expenditures only decreased by 4.6%, suggesting a 1% increase in inferred freight rates.

The inferred rate index dipped 6.2% from January (4.9% decrease when seasonally adjusted), affected by a lean towards more economical freight modes. The report notes potential for freight rates to see low- to mid-single-digit growth in 2025 after a 7% drop in 2024.

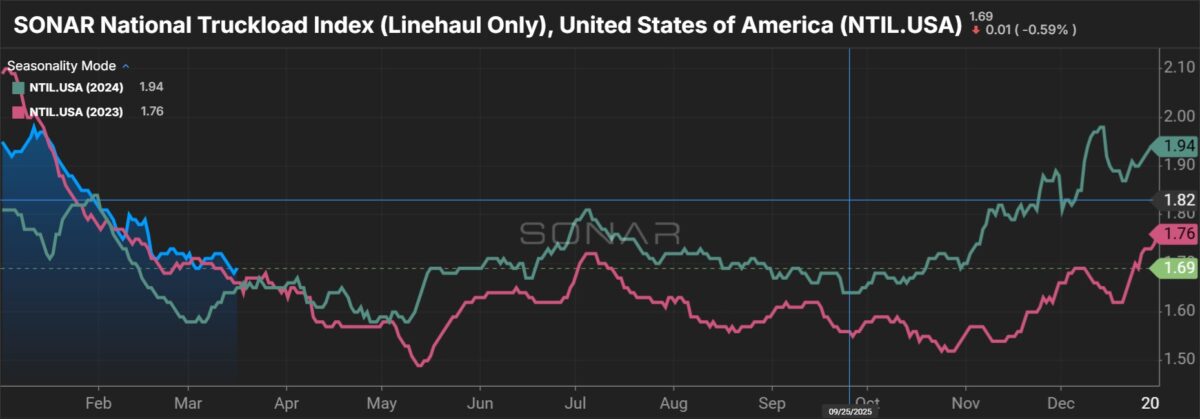

The Truckload linehaul index, excluding fuel and other surcharges, recorded its sixth consecutive monthly rise in February with a 1.2% increase month-over-month and a 1.9% year-over-year rise.

The NTIL is an average of booked spot dry van loads from 250,000 lanes, showing trends for 2025.

Market Outlook: Caution Amid Uncertainty

The freight market faces a challenging outlook; trade tariffs and economic uncertainties could disrupt demand. However, there's a silver lining for for-hire freight markets, especially as increased recession risks may limit private fleet capacities. If current standards remain unchanged, tractor prices might surge by $20,000 per unit once the USMCA exemption concludes, potentially elevating freight rates further.

Data leveraged in Carr's report stem from immense volumes of freight bills processed by Cass Information Systems (NASDAQ: CASS). They manage $36 billion in freight payables annually.

Read more insights on these topics: